Payment history: The ultimate guide to your credit scores

Summary

- Payment history is a key factor in both personal and business credit scoring models.

- Personal credit reports use 30-day increments to track late payments, while business credit reports often use “days beyond terms” for more detailed tracking.

- Factors like payment history, credit utilization, or length of credit history all may help determine your overall creditworthiness.

- Setting up automatic payments and monitoring your credit reports regularly can help track your progress and catch mistakes quickly.

Editorial note: Our top priority is to give you the best financial information for your business. Nav may receive compensation from our partners, but that doesn’t affect our editors’ opinions or recommendations. Our partners cannot pay for favorable reviews. All content is accurate to the best of our knowledge when posted.

“The delivery guy, he changed our terms. We went from a net-45 to a net-30 which just, like, sucks, you know? Because I was about to ask him if we could move to a net-60,” said Mikey, the owner of the restaurant The Bear in the TV series of the same name.

“So instead of having that lovely conversation, now we got to talk about a payment plan.”

Even though Mikey is a fictional character, his struggle is real. Maybe as a small business owner, you’ve been in his shoes — going through a time when cash flow is tight and you need more time to pay your suppliers.

This guide is designed to help you understand how payment history impacts your credit and how to avoid and navigate potential problems.

How payment history impacts your credit scores

Here's a breakdown of the different ways that payment history may affect your personal and business credit scores.

Personal credit

When it comes to your personal credit reports, payments are categorized into 30-day buckets: on time or current; or 30, 60, 90, or 120 days late. This means most personal lenders will not report a late payment on an account unless it is a full billing cycle (30 days) or more past due.

For example, if your credit card bill is due on January 2nd, your payment typically won't be reported as late as long as it's received and credited to your account by February 1st.

That said, you may still be charged a late fee if you're even a few days late. And in some cases, creditors can report missed payments immediately. So your best bet is to pay on time every time.

Business credit

Business credit works somewhat differently.

Rather than reporting payment activity only in 30-day increments, business credit reports often use days beyond terms (DBT). This system tracks exactly how many days past your agreed payment terms you paid an invoice.

Here's how it works:

- Let's say your payment terms with a vendor are net-20, meaning the balance is due 20 days after the invoice date.

- If you pay 22 days after the invoice date, your account is two days beyond terms, and may be reported as 2 DBT.

- If you pay 45 days after the invoice date, that's 25 DBT.

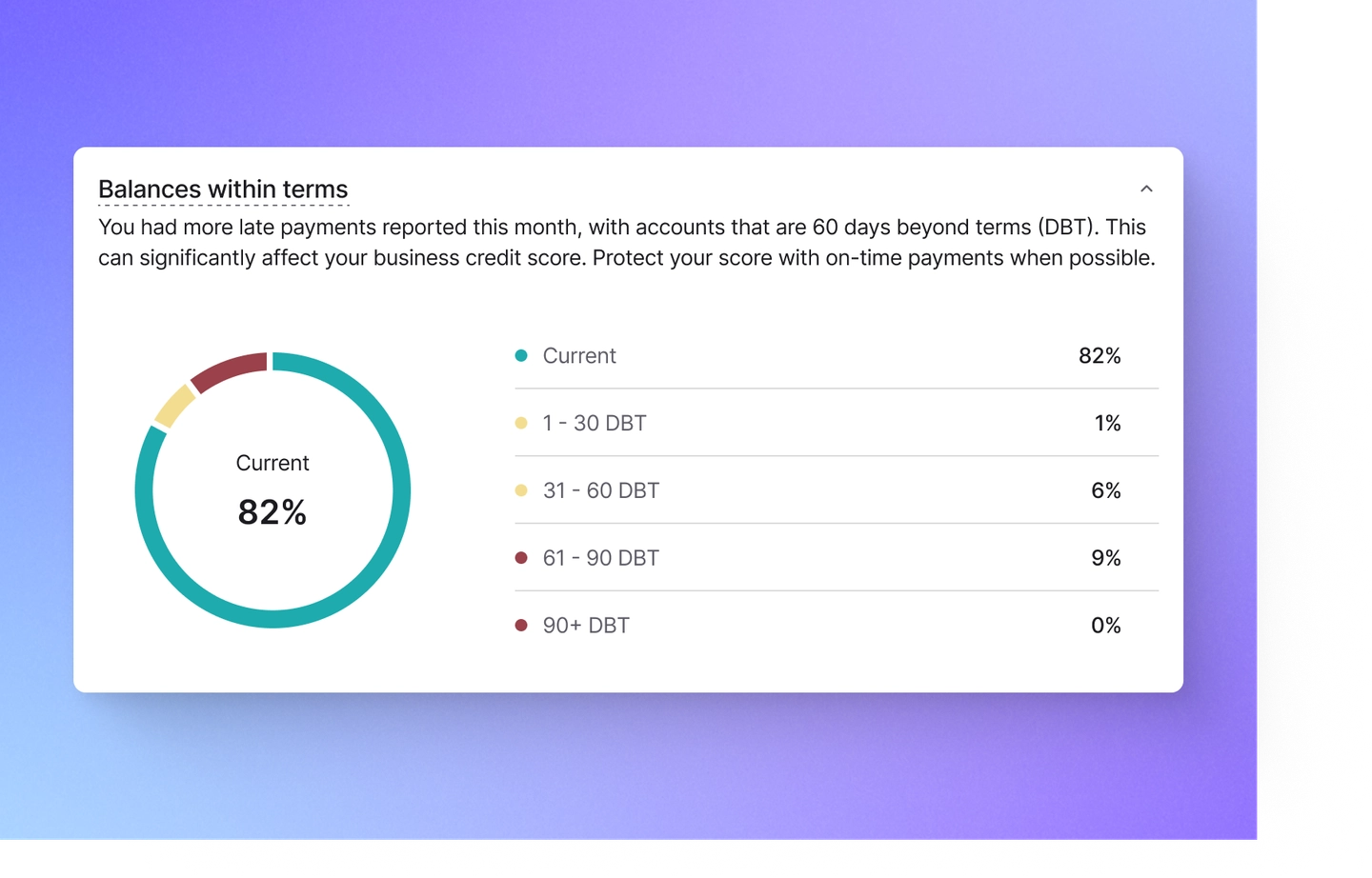

When you connect your accounts to Nav's Credit Health tool, you can see the percentages of your balances within terms (or the number of accounts that are paid on time). Here's what it looks like:

How severity, frequency, and recency affect your score

Credit scoring models evaluate late payments in several ways, and each dimension can carry its own weight in how much your score may drop.

Severity: How late were you?

Scoring models often take into account the severity of late payments. A payment that's 90 days late will likely hurt your scores more than one that's 30 days late, for example. The longer you go without paying, the more that late payment impacts your scores.

Frequency: How many times were you late?

The number of late payments matters. One missed payment can affect your scores, but a pattern of multiple late payments signals chronic payment problems. If you have several accounts showing late payments, your credit scores will typically suffer more than just one isolated incident.

Recency: How recently were you late?

Recent information tends to carry more weight in credit scoring models. Late payments in the last two years will generally have a greater impact on your scores than older late payments. As late payments age, they may hurt your scores less severely, especially if your payment history has been strong since then.

The impact on high scores

Here's something that surprises many people: the better your score to begin with, the more it may drop due to a reported delinquency.

Why? Because high scores usually are associated with on-time payments and other positive credit habits (like low debt, and a good credit mix). A single late payment disrupts that pattern and signals to scoring models that something may have changed in the person's financial situation. For someone with a lower score who may already have some negative marks, one more late payment doesn't represent as dramatic a shift in their credit profile.

The good news is that people with high scores often recover more quickly. As a general example, if you had a score of 780 and dropped to 670 after a late payment, you may be able to rebuild your credit faster than someone starting from a lower baseline, assuming you return to consistent on-time payments.

See detailed examples of how late payments may affect your scores at MyFICO.com.

5 strategies to improve your payment history

Building a positive payment history takes time, but you can take concrete steps today to potentially start improving your credit profile.

1. Set up automatic payments

Automatic payments can be one of the most effective tools for protecting your payment history. Most creditors offer autopay options that pull the minimum payment (or full balance) from your bank account on the due date.

You can typically choose to pay the minimum amount, a fixed amount, or the full statement balance. Even if you prefer to pay manually most of the time, setting up autopay for at least the minimum payment provides a safety net in case you forget or get busy.

2. Use payment reminders

If you don't want to use automatic payments, set up reminders well before your due dates. Most banks and credit card companies offer email or text alerts when bills are due. You can also set reminders in your phone calendar or use a financial app that tracks all your bills in one place.

Set your reminders for a few days before the due date, not on the due date itself. This gives you time to handle any unexpected issues, like needing to transfer funds between accounts or dealing with a payment that doesn't get processed immediately.

3. Budget to avoid cash flow gaps

Sometimes late payments don’t happen because you forgot to make a payment, but because they didn't have the funds available when the bill came due. Try to build a cash buffer to cover at least one month of expenses, so seasonal fluctuations don't force you into late payments.

4. Focus on rebuilding after late payments

If your credit report lists delinquencies that are accurate, try to pay on time going forward. With most credit scoring models, recent information carries significant weight.

While a late payment can stay on your personal credit reports for up to seven years, as your late payments age, they may hurt your scores less severely — especially if your payment history has been strong since then.

5. Dispute inaccurate late payments

If you spot late payments on your credit report that you believe are incorrect, you have the right to dispute them. You can file disputes directly with the credit bureaus online, by mail, or by phone.

The credit bureau will investigate by contacting the company that reported the information. With consumer credit reports, if the credit bureau cannot verify the late payment, it must remove it from your report. This process typically takes up to 30 days.

Business credit bureaus aren’t required to dispute payments within a specific time frame, but will usually follow a similar timeline.

If your dispute is successful and the late payment is removed, you may see an improvement in your credit scores that’s sometimes specific.

Learn how to dispute mistakes on your credit reports with Nav’s guide.

Payment history in business credit scores: key differences

When it comes to business credit reports and scores, payment history is treated differently from personal credit. Understanding these differences can help you manage your business credit more effectively.

Days beyond terms: a more granular approach

Earlier, we mentioned that business credit bureaus often track days beyond terms (DBT).

This detailed tracking means even small delays can show up on your business credit report. Unlike personal credit — where you might have almost 30 days of leeway before a late payment is reported — with business credit, being just a few days late can be noted.

The average DBT across all businesses is seven days, according to Experian. This means many businesses routinely pay a week after their terms, but paying on time or even early can help you achieve higher scores.

How different bureaus weigh payment history

Payment history can make up anywhere from 50% to 100% of your business credit score, depending on which business scoring model is being used. This means it typically carries a lot of weight in business credit scores, and sometimes even more than with personal credit scores, where it's one of several significant factors.

Dun & Bradstreet

The Dun & Bradstreet PAYDEX® Score, for example, ranges from one to 100 and is based on your payment performance. It takes into account current DBT, average DBT, and highest DBT across all reporting trade accounts. The score also uses dollar-weighting, meaning larger invoices typically carry more weight in the calculation than smaller ones.

Experian

The Experian Intelliscore PlusSM uses payment history as a primary factor but also incorporates other data points like credit utilization, public records, and company information. This scoring model can range from 1–100 (for versions 1 and 2) or 300– 850 (for version 3), It also offers the option to blend personal credit information with business credit data.

Equifax

Equifax business credit scores also place significant emphasis on payment history, using DBT information in their calculations. They offer several different credit score models, including the Equifax Business Delinquency Score®, and Equifax Business Failure Score®, each weighing payment patterns differently based on what they're predicting.

The bottom line, though, is that payment history matters. On-time payments can help build good credit and late payments can hurt your scores.

The early payment advantage

Here's something unique to business credit: While late payments can hurt your scores, early payments may help you achieve a higher score with some scoring models. This is different from personal credit, where paying early doesn't typically boost your scores beyond paying on time.

To earn the highest D&B PAYDEX® Score of 100, for example, a business needs to have sufficient credit references that report to D&B, then pay consistently before the due date. (While a business may achieve a higher D&B PAYDEX® Score by consistently paying invoices before their due date, outcomes may vary depending on data reporting and weighting.)

Less severe individual impact

Because business credit reports track payment information so granularly, a single late payment out of many is not as likely to drop your scores dramatically as it would with personal credit. If you have 50 tradelines reporting and one shows 15 DBT while all the others show on-time or early payments, the impact may be somewhat diluted across your overall payment pattern.

The projected DBT for all U.S. businesses is 80% of U.S. businesses have a DBT of 0–15 days; 11% of U.S. businesses have a DBT of 16–50 days. The rest pay even later on average.

Consistent late payments will catch up with you, and a pattern of late payments can significantly hurt your business credit scores.

Blended scoring models

Some business credit scoring models can evaluate both personal credit data as well as business credit data. Examples of these blended scores can include:

- FICO® SBSSsm Score

- Experian Intelliscore PlusSM

- Equifax Business Delinquency ScoreTM

- Equifax Business Delinquency Financial ScoreTM

This means that your personal payment history may also affect your business credit scores in some cases. If you're a new business owner with limited business credit history, having strong personal credit may help your business qualify for small business financing.

As your business builds its own credit history, scoring models may rely more heavily on the business data.

Watch: Personal credit vs. business credit & the difference no one talks about

How payment history works with other credit factors

Payment history works together with other credit score factors to evaluate creditworthiness. Understanding how these factors interact can help you make better decisions about how you manage your credit.

Credit utilization

Credit utilization measures how much of your available credit you're using. For personal credit, this is typically calculated by dividing your total credit card balances by your total credit limits. For business credit, it may compare your balances with your recent high balances, since credit limits aren’t often reported.

Length of credit history

The length of time you've had credit accounts matters to scoring models. A longer credit history gives lenders more data to evaluate your payment patterns. With personal credit, this includes the age of your oldest account, the age of your newest account, and the average age of all your accounts.

For business credit, the length of time your business has been established and how long you've had relationships with reporting vendors and creditors can be a factor in some scoring models. A new business with just six months of perfect payment history may score lower than an established business with five years of perfect payment history, all else being equal.

Credit mix

Credit mix refers to the variety of credit types you have. For personal credit, this might include credit cards, auto loans, mortgages, and personal loans. For business credit, it might include business credit cards, equipment loans, lines of credit, and trade credit accounts.

Having a diverse mix of credit types can often benefit credit scores, though this is typically a less important factor than payment history or utilization.

But that doesn’t mean your business should open new types of accounts and go into debt just to improve your credit mix. Use credit and debt only when it meets a business need.

Recent credit inquiries and new accounts

When you apply for new credit, it typically results in a hard inquiry on the credit report where the credit check took place. Too many hard inquiries in a short time can lower your scores slightly, as it may signal that you're taking on too much new debt.

New accounts may also affect the average age of your credit history, which may temporarily lower your scores. However, if you pay on time, the long-term benefit usually outweighs the short-term dip.

For business credit, inquiries are often tracked differently than with personal credit. Some business credit bureaus don't factor inquiries into their scores at all, while others may consider them as a minor factor.

Public records

Public records like bankruptcies, tax liens, and judgments can severely damage your credit scores, as they are associated with high risk. However, tax liens and judgments don’t normally appear on consumer credit reports. They can appear on business credit reports.

For business credit, UCC filings (which indicate secured loans) may also appear on your credit reports. While UCC filings themselves aren't necessarily negative, multiple UCC filings or high total exposure can raise concerns for lenders evaluating your business.

Frequently asked questions

Rate this article

This article currently has 30 ratings with an average of 5 stars.

Gerri Detweiler

Education Consultant, Nav

Gerri Detweiler has spent more than 30 years helping people make sense of credit and financing, with a special focus on helping small business owners. As an Education Consultant for Nav, she guides entrepreneurs in building strong business credit and understanding how it can open doors for growth.

Gerri has answered thousands of credit questions online, written or coauthored six books — including Finance Your Own Business: Get on the Financing Fast Track — and has been interviewed in thousands of media stories as a trusted credit expert. Through her widely syndicated articles, webinars for organizations like SCORE and Small Business Development Centers, as well as educational videos, she makes complex financial topics clear and practical, empowering business owners to take control of their credit and grow healthier companies.