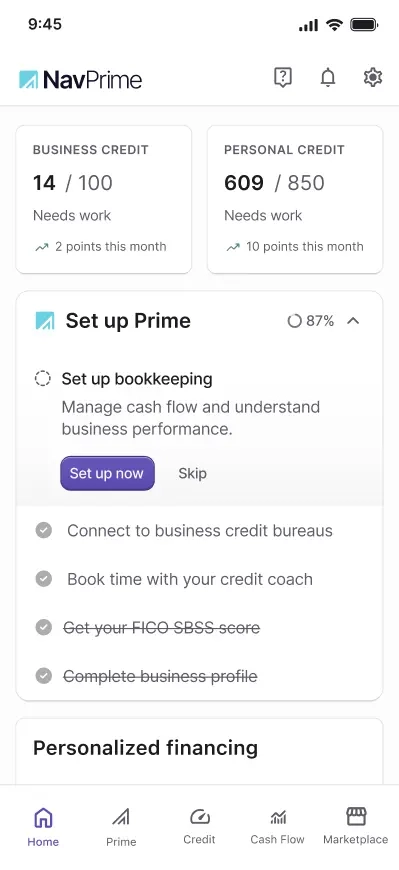

Business credit, made better

Monitor and build business credit with all 3 major business bureaus so you can unlock your brightest business days. You can check your credit standing for free.

YOUR MEMBERSHIP

Invest in your success

Getting credit reports elsewhere would cost you 4x more each month.1

Pay monthly

Pay quarterly

save 20%

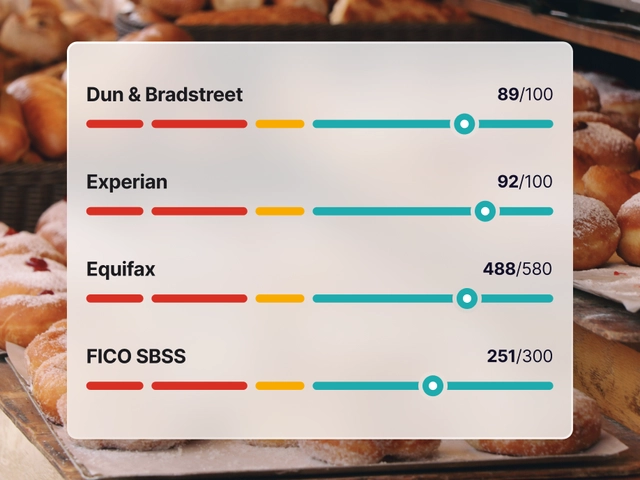

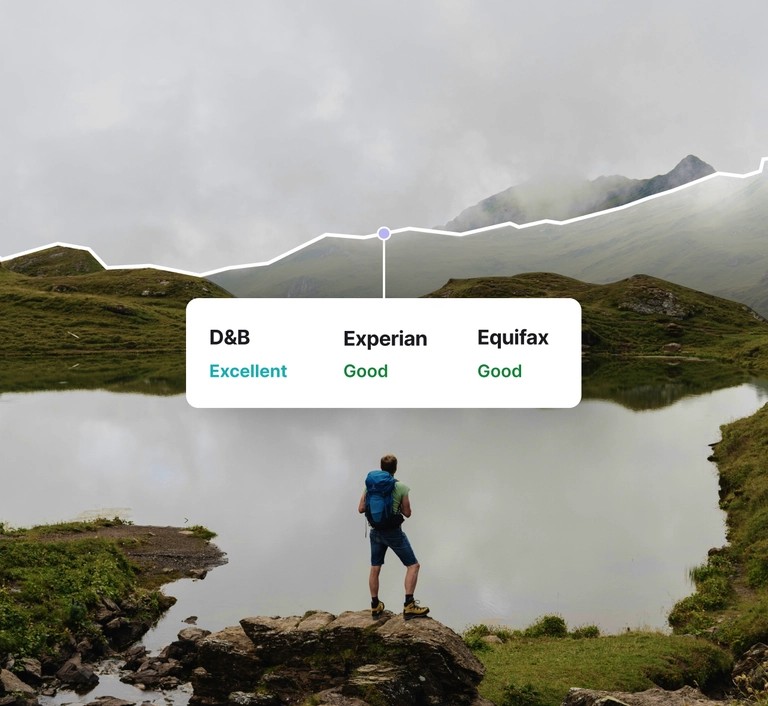

5 credit scores, alerts, and reports from D&B, Experian, Equifax, and TransUnion

Exclusive discounts on fees from Nav’s trusted lending partner2

Build

Popular$49.99

/ mo

For growing businesses looking to build business credit with up to 2 tradelines³

Build with Prime5 credit scores, alerts, and reports from D&B, Experian, Equifax, and TransUnion

Exclusive discounts on fees from Nav’s trusted lending partner2

One tradeline to build business credit (membership payment)

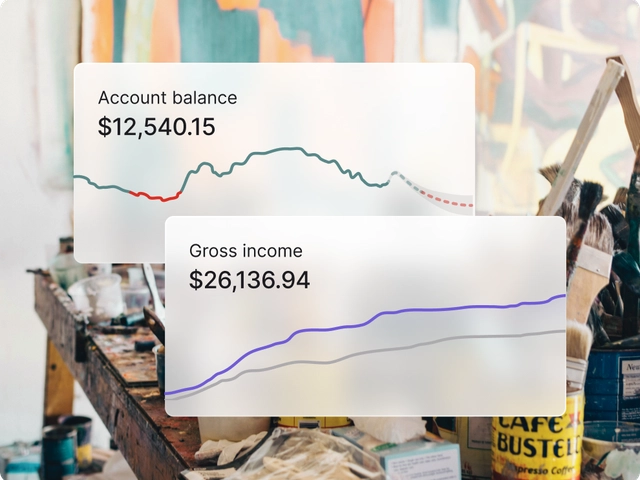

Bookkeeping tools to manage cash flow and simplify tax prep

Coming soon: Nav Credit Builder Card4 with a second tradeline opportunity (not included at signup)

5 credit scores, alerts, and reports from D&B, Experian, Equifax, and TransUnion

Exclusive discounts on fees from Nav’s trusted lending partner2

One tradeline to build business credit (membership payment)

Bookkeeping tools to manage cash flow and simplify tax prep

Coming soon: Nav Credit Builder Card4 with a second tradeline opportunity (not included at signup)

Business Credit Coaching

FICO SBSS score to track eligibility with 7,500+ lenders — and the SBA