Find your path to small business growth

Get your business ready for funding. Monitor and build business credit and take steps to help strengthen your eligibility.

everything you need

Driving your business forward

Know where you stand, find options that fit, and plan your next steps. Nav isn’t just a powerful suite of financial tools — we’re part of your team.

YOUR MEMBERSHIP

Nav Prime unlocks powerful support for your business

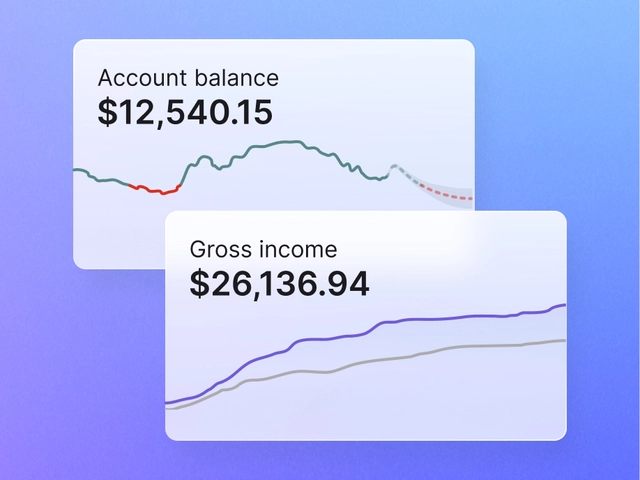

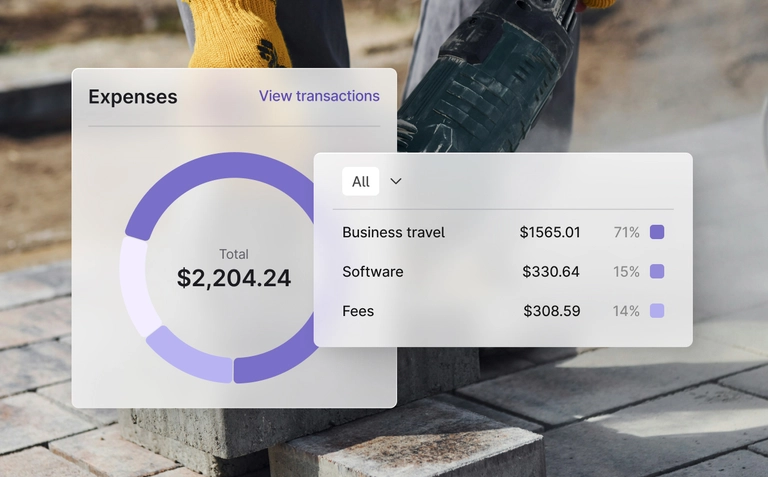

Track credit, cash flow, and your eligibility for funding in real time. Getting credit reports elsewhere would cost you 4x more each month.1

Pay monthly

Pay quarterly

save 20%

Free

$0

/ mo

For businesses seeking a general idea of their funding readiness and approval odds

Sign up for freeFree features

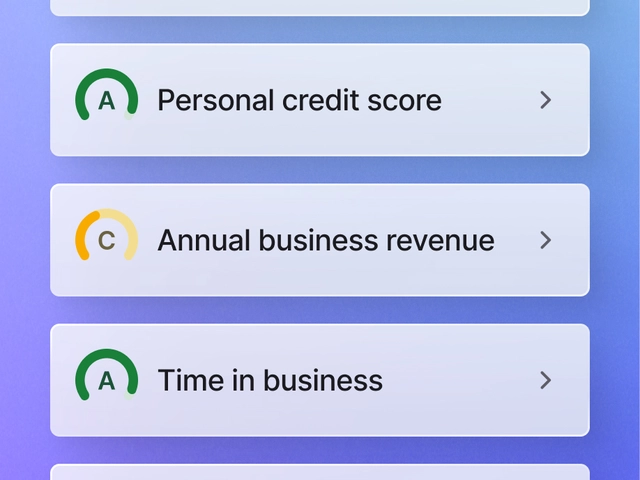

Basic funding readiness summary for loans, credit cards, and trade credit

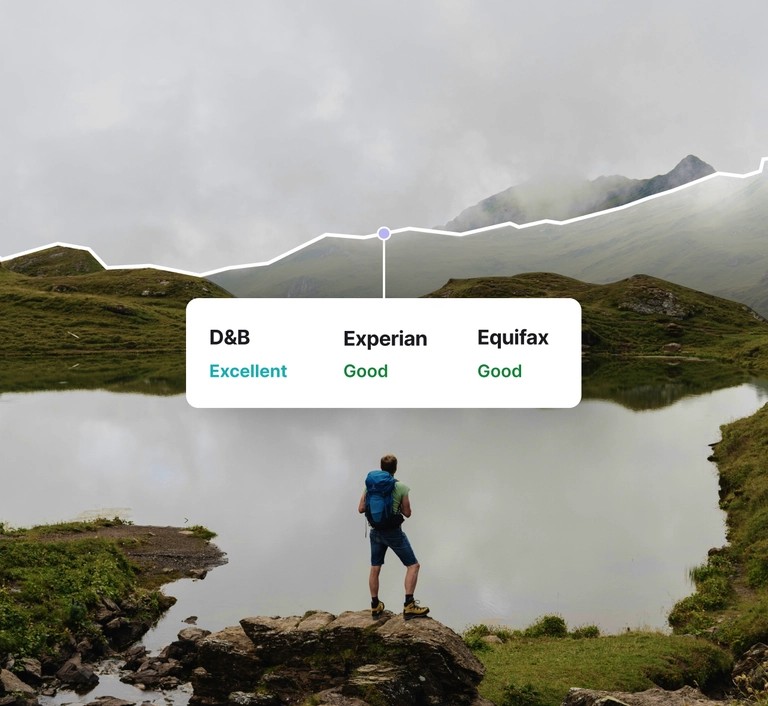

Basic business credit range and high level data from the major bureaus

1 personal credit score and report from Experian

Basic cash flow tracking across unlimited accounts

Track

$39.99

/ mo

For businesses who want to understand and monitor their current funding readiness

Join Nav PrimeEnhanced features with Track

Funding readiness assessment for loans, credit cards, and trade credit

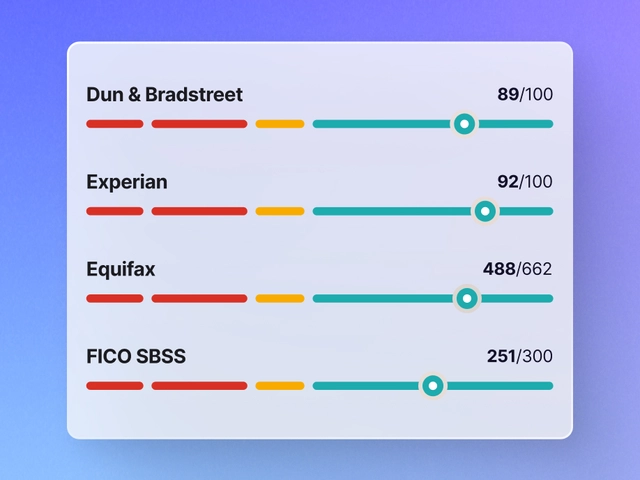

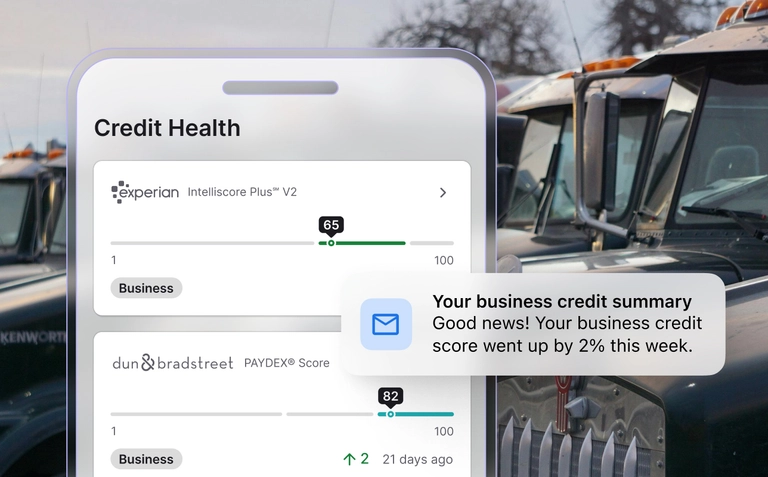

Business credit scores, reports, and alerts from the major bureaus

2 personal credit scores and reports from Experian and TransUnion

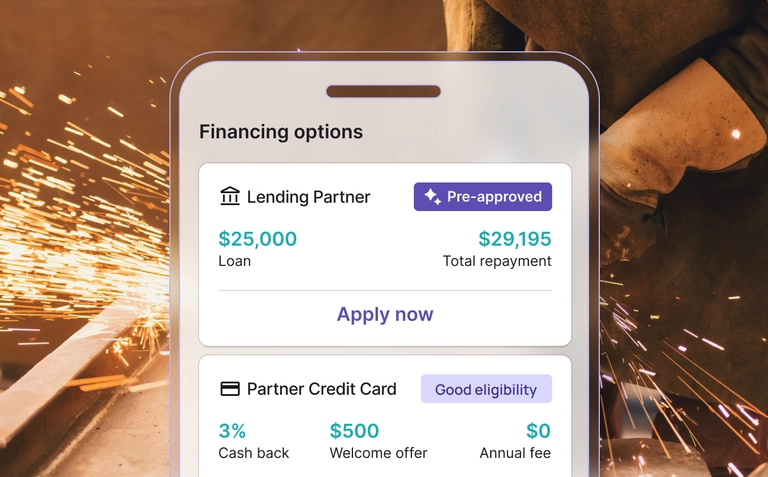

Exclusive discounts on fees from Nav’s trusted lending partner2

Build

$49.99

/ mo

For businesses looking to build business credit to help improve their funding readiness

Join Nav PrimeEnhanced features with Build

Tradeline to build business credit3 (membership payment)

Funding readiness assessment for loans, credit cards, and trade credit

Bookkeeping tools to manage cash flow and simplify tax prep

Coming soon: Nav Credit Builder Card4 with a second tradeline opportunity (not included at signup)

Expand

$74.99

/ mo

For businesses who want 1-on-1 guidance to help maximize their funding readiness

Join Nav PrimeEnhanced features with Expand

Tradeline to build business credit,3 plus Business Credit Coaching

Monthly coaching to break down your action plan for funding readiness

FICO SBSS score to track eligibility with 7,500+ lenders

Coming soon: Nav Credit Builder Card4 with a second tradeline opportunity (not included at signup)

Free

$0

/ mo

For businesses seeking a general idea of their funding readiness and approval odds

Sign up for freeFree features

Basic funding readiness summary for loans, credit cards, and trade credit

Basic business credit range and high level data from the major bureaus

1 personal credit score and report from Experian

Basic cash flow tracking across unlimited accounts

Pay monthly

Pay quarterly

save 20%

Track

$39.99

/ mo

For businesses who want to understand and monitor their current funding readiness

Join Nav PrimeEnhanced features with Track

Funding readiness assessment for loans, credit cards, and trade credit

Business credit scores, reports, and alerts from the major bureaus

2 personal credit scores and reports from Experian and TransUnion

Exclusive discounts on fees from Nav’s trusted lending partner2

Build

$49.99

/ mo

For businesses looking to build business credit to help improve their funding readiness

Join Nav PrimeEnhanced features with Build

Tradeline to build business credit3 (membership payment)

Funding readiness assessment for loans, credit cards, and trade credit

Bookkeeping tools to manage cash flow and simplify tax prep

Coming soon: Nav Credit Builder Card4 with a second tradeline opportunity (not included at signup)

Expand

$74.99

/ mo

For businesses who want 1-on-1 guidance to help maximize their funding readiness

Join Nav PrimeEnhanced features with Expand

Tradeline to build business credit,3 plus Business Credit Coaching

Monthly coaching to break down your action plan for funding readiness

FICO SBSS score to track eligibility with 7,500+ lenders

Coming soon: Nav Credit Builder Card4 with a second tradeline opportunity (not included at signup)